This is the second in a series of posts about creating and utilizing a great program-centered budget. Click here for a link to the first.

Introduction

“Don’t tell me what you value; show me your budget, and I’ll tell you what you value.”

A nonprofit’s annual budget has the capacity to be the most important communication tool the organization has – both internally and externally. A clear and purposeful budget can simultaneously provide trustees and staff the insights and understanding they need make mission-driven strategic decisions and inspire donors, program partners, and other constituents to engage with the organization.

A great budget tells a story about what we value – every bit as much as a great speech, brochure, website, or solicitation. When we develop a budget, it’s our obligation, and a great opportunity, to tell that story intentionally and directly – and (importantly) in a way that doesn’t make most readers feel like they’re reading a foreign language. I believe that the most compelling and effective way to do just that is through a “Program-Centered Budget.”

* * * * *

Part II: Choosing the Right Revenue and Expense Lines

(and Naming Them Well)

I’ll be frank and share that, as I wrote the very-dry and very-in-the-weeds beginnings of this second post in the series, I almost deleted post #1 and scrapped this whole idea – worried that a more boring title and topic would be hard to find. But I do think that this topic is important, so I’ve decided to dig in. That said, it seems advantageous to keep us all engaged with photos of a puppy I think is basically irrisistable - a Pomeranian/Husky mix - THE POMSKY. You’re welcome.

Pomsky Puppy Asks: “What are some things to consider when naming revenue and expense lines on a nonprofit budget?”

Thanks, for asking, Pomsky Puppy.

Let’s look at expense and revenue lines for the Summary Budget – the top-level budget that is most frequently reviewed by the full board and most frequently shared when a donor or other external constituent is shown our budget. (This is also the budget that tends to tie most directly to our annual Audited Financials.)

Quick Recap: Program-Centered Budgeting Part I

A Program-Centered Budget organizes itself around the primary programs (mission-focused activities) that the organization offers or undertakes. All shared expenses, from office supplies up to the chief executive’s salary, are allocated to either (1) one of the organization’s core programs/activities; (2) fundraising costs; or (3) G&A. Click here to review "Choosing to Create a Program-Centered Budget."

Expense Lines in the Summary Budget

We’ll always want to include independent line-items for Fundraising and G&A, which is pro forma – expected on any budget. (In the future installment about allocations, we’ll talk about not “over-counting” either of these – something that happens a lot.) For the other top-level expense lines, this is where we want to think about what we’re trying to communicate – what is the story we’re telling. The right expense-line names will be driven by our specific mission, constituency/community, strategic priorities, etc. By choosing a Program-Centered Budget, we’ve already agreed that the “core programs” will be our expense lines. But we have good story-telling decisions to make about how we present our core programs (what do we consolidate and what do we break out) and what language we choose to make our story as evocative and compelling as possible.

Let’s use an example of a theatre company that already utilizes a Program-Centered Budget. (It’s from a real organization that has it’s financials online; for our purposes, I’m changing their name to ABC Theatre.) They present their expenses as follows:

For all of the reasons outlined in Part I of this series, this approach is already much better than a Departmental or Functional budget. Q: What does the organization do? A: Performances and Education. But there are opportunities to break out and rename the program services that would tell both internal and external readers more about what the organizations values and accomplishes. Consider this alternative to this same budget:

We know much more about Theatre X from this presentation of the same bottom-line expense numbers. We know that they have two stages, one of which is primarily about experimentation. We know that they spend a lot more on main stage productions than they do on their experimental stage, but that they are still committing serious funding to experiential theatre. And we know that they have two primary types of educational programs – bringing students to the theatre for productions and going into classrooms to do work with children at school.

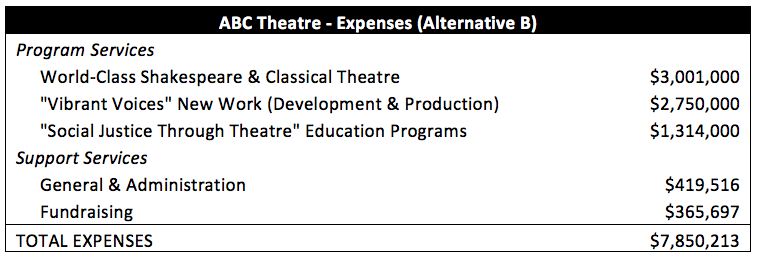

Or we can consider a different focus for the theatre...

Once again, the way they break out the expense lines (vs. just "Performances and Education" tells us a lot about the mission, focus, and work of this version of ABC Theatre. We know that they do two basic kinds of theatre – Shakespeare & Classical and New Work. Going deeper, we also know that they are doing “world-class” Shakespeare and Classical theatre, which tells us something about the level of actors, directors, designers, and full-productions audiences experience. We know that they spend almost as much money on development and production of New Work as they do on Shakespeare and Classical work. The name of their new work program, "Vibrant Voices," gives us a some insight about the focus and aspiration of the new work they create, and we know know that they invest in both production of new work and development of new work (presumably with the possibility of it being produced in future years). We know the primary focus and purpose of their education programs is to explore social justice through theatre – as opposed to other purposes such programs might have, such as gaining confidence, building teamwork skills, developing a general appreciation for theatre, etc. (Many organizations already have excellent and evocative names for their programs that can be placed directly into their budgets. If you have an evocative name, it's almost always a good idea to use it.) For all three of the expense lines under “program services,” we are given a sense of what they’re trying to accomplish, why it matters, and implicitly why it’s worth supporting philanthropically.

Pomsky Puppies say: “But Sean, we don’t work at a theatre. We work at a museum, a social service organization, a conservation organization, a hospital, a social justice organization, and a homeless shelter – respectively. What about us?”

Don’t worry, Pomsky Puppies. This approach works for all of you. No matter what the purpose of your nonprofit, you all exist to serve your community and/or constituents. You all exist solely to create public benefit. Whatever core programs you offer to create that benefit, those are your expense lines – and you can follow the considerations laid out in our theatre example above to help develop the clearest and most evocative way to categorize and describe those programs.

Revenue Lines in the Summary Budget

Big picture, we want people to look at the revenue section of our budget and have a clear understanding of where the money comes from to fund our work to achieve our mission (as articulated in the expense section of the budget). Most of the work to create an evocative and compelling message comes on the expense side, so there is less work needed for revenue lines to get the “poetry” of the language right. But we still have opportunities to decide what we want to communicate, and why. A straightforward (minimalistic) approach could look like:

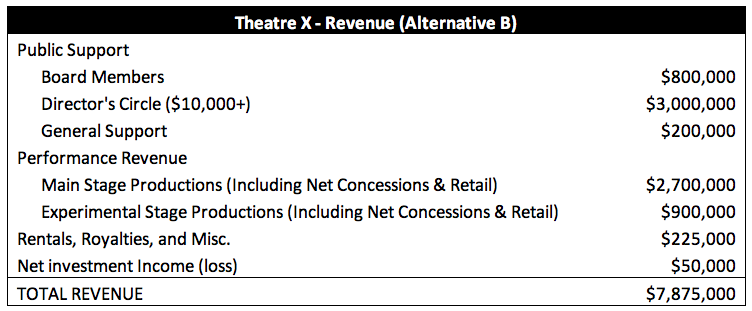

But, like expenses, we can break things out in a way that conveys what we want people to know (what we think it’s important to track on this highest-level budget). You’ll note that in all of the following examples, what is called out is telling about the organization’s focus and priorities.

All three alternatives show valid approaches. It’s all about what the organization values and wants to convey – perhaps to correct a misperception, perhaps to reinforce something positive that is already generally accepted, perhaps to call-out something we’re working to change over time. (Note: Looking at Alternative C, there should be a really good reason that you’re calling out restricted/designated gifts. But that’s my inclination based on my approach to development; the point is, you know your organization best, and the lines need to reflect your priorities.) The important thing is to make the naming clear, thoughtful, and intentional.

Detailed (Second-Level) Budgets

Of course, behind every line on the Summary Budget is a great deal of supporting detail on a second-level Detailed Budget. Even on those sub-budgets, think about how you’re naming each revenue and expense line. How are you tracking and telling the financial story of each core program and each source of revenue?

Pomsky Puppy Says: “Thanks, Sean. I can’t wait to start trying this. It's great to think of our budget as a tool in our communications arsenal. It’s going to be thought-provoking and engaging to look at how we can match our budget-line naming to our core purpose and compelling messaging.”

Well thank you for saying that, Pomsky Puppy. I think you’ll be happy with how this develops.

In the next installment of this series (Part III), we’ll take an in-depth look at how to analyze and allocate shared expenses. Additional baby animal photos will be needed.